Is the economy really as hot as the unemployment rate says it is? Nup.

So everyone was all cock-a-whoop about the jobs data last week.

(Yeah, I just wanted an excuse to use ‘cock-a-whoop’. New favourite expression.)

But they were. “Astounding”, “Dazzling”, “Impressive”.

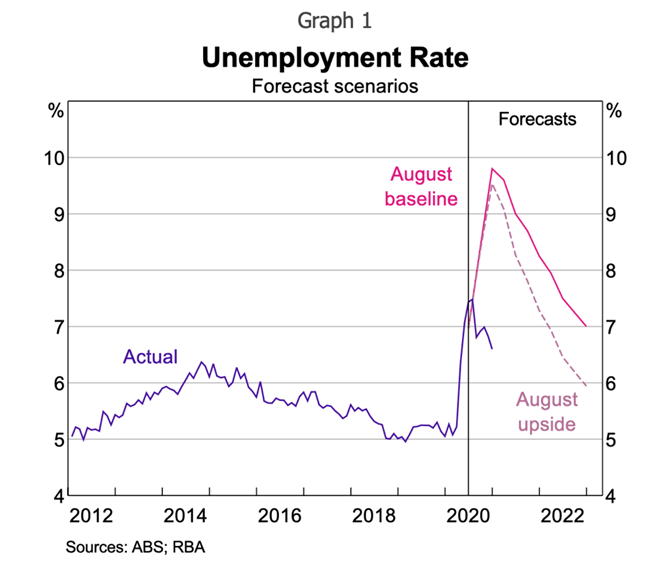

And look, on the face of it, it was a very strong result. The unemployment rate took a bit lurch downward, from 5.5% to 5.1%. Massive.

What’s more, that came with impressive jobs growth – not in part-time work either – but in full-time work.

So it looked like a very strong result.

And at 5.1%, we’re now very close to the all important 5% threshold.

The RBA have said they need to see unemployment with a four in front of it before they even start thinking about raising rates. Frydenberg wants to see something in the mid-4s.

So we’re almost there right? Job done. Put the pandemic recovery kit away. Right?

But not so fast.

You see, it seems that immigration is playing havoc with the numbers.

Or the lack of immigration to be precise.

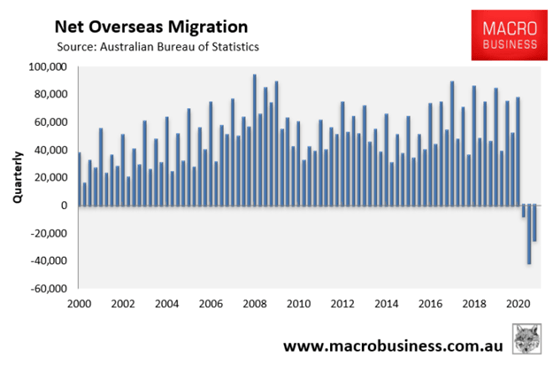

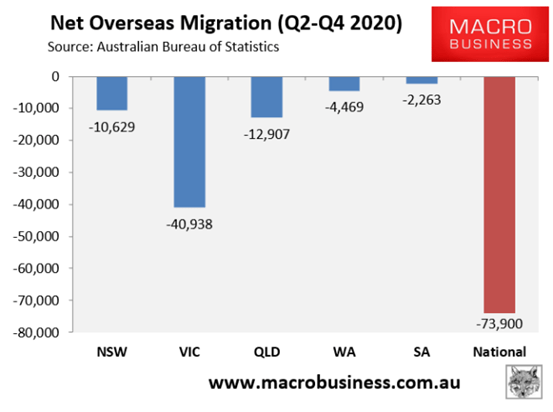

Net immigration has gone negative.

And we’ve now lost 73,000 people since Covid began:

With the majority of those exiting Victoria.

(Aw, c’mon guys. It’s not so bad. Come back!)

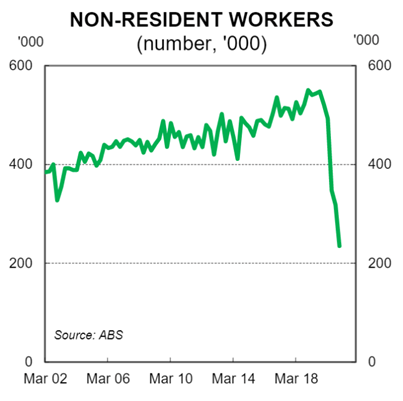

This fall in immigration has coincided with a big fall in the number of non-resident workers. We’ve seen a sizeable 334,000 non-residents leave the country and leave the workforce.

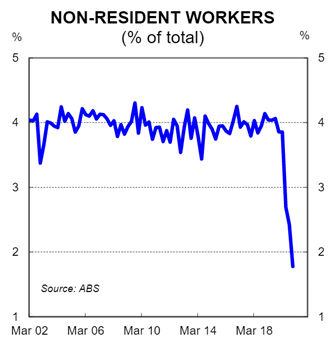

Their share of the workforce has fallen from around 4% to under 2%.

And it seems that the jobs these non-residents are giving up are being filled by locals.

That’s good for locals, but it does mean it’s making the jobs data look better than it is.

Because with these jobs, we’re not talking about a growing economy generating new jobs. Or a recovering economy recreating lost jobs as new jobs.

Rather we’re talking about old jobs being made vacant by exiting immigrants, and locals filling the spot.

And that means that our current unemployment rate might be making the economy look better than it is.

How much better? That’s hard to say.

Chris Joye at the AFR crunches the numbers and he reckons that if we hadn’t had this non-resident exodus, the unemployment rate might be stuck around 7.5%:

If one assumes the 333,900 non-resident jobs are all placed with locals who were looking for work (and not folks who are sucked into the labour market), this has the effect of temporarily reducing our unemployment rate by 2.4 percentage points.

Put another way, if borders open and non-resident workers return and take these jobs, the unemployment rate would increase from 5.1 per cent to 7.5 per cent. Although this is a very crude upper bound, it gives a sense of the influence of the non-resident worker exodus on the jobless rate.

So this takes quite a lot of gloss off the jobs numbers. Where we had been thinking that the economy was tearing along and creating new jobs everywhere, it might not be exactly like that.

The recovery may in fact be a lot more modest than all that.

So this should give the markets and the RBA pause for thought.

The recovery is still going well, but let’s not be too hasty to turn the garden hose on it just yet.

JG