REA Group is giving us an insight into property demand. And it’s simply scorching.

I’m sure you don’t need to be told this if you’re active in the market right now, but property demand is red-hot right now.

Like scorching.

That’s the read we’re getting from REA Group – the mob behind realestate.com.au.

They reckon they’re seeing huge volumes of buyers across their websites – at levels miles above what they were seeing pre-Covid.

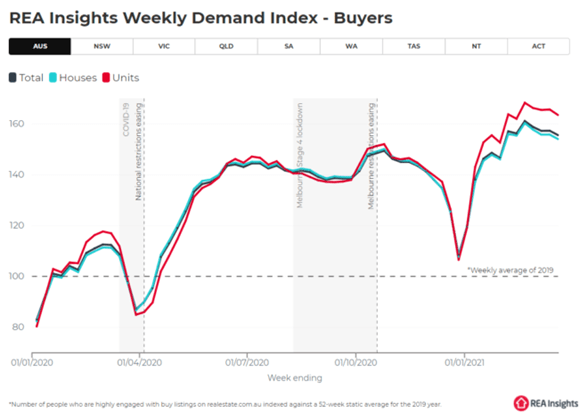

This is what their demand index for buyers shows. Demand bounced back incredibly strongly out of Covid, and has been very elevated since.

I reckon what this shows is how much pent up demand was in the market – how many people were hoping for a bargain to be able to get into the market. That’s why search activity was so quick to launch.

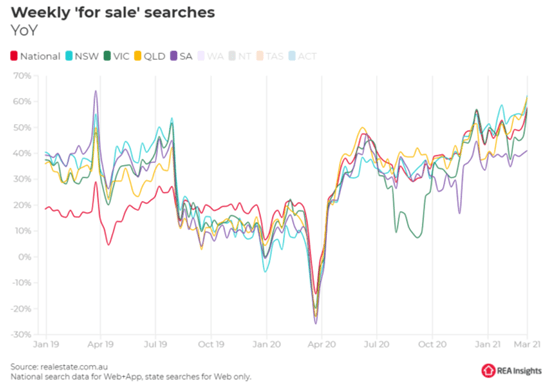

It’s a similar story in the ‘for sale’ searches, with all states coming back in a big way.

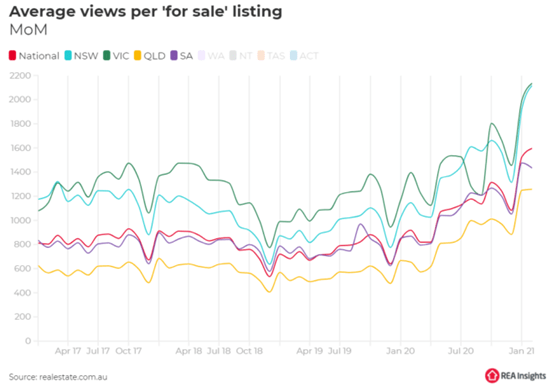

Average views per listing have gone through the roof, which probable reflects how little stock is on the market right now.

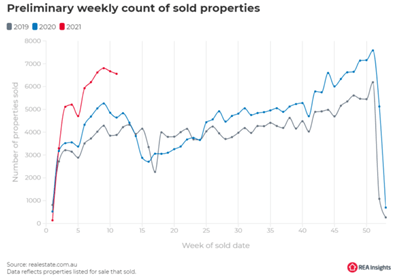

And stock is down mostly because a spike in successful sales activity is chewing through the available housing stock. Sales are well up on previous years.

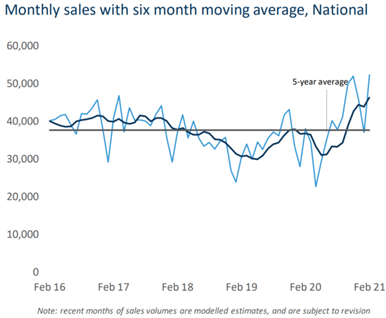

You get a sense of that from Corelogic’s sales data too, which is well above its 5-year average.

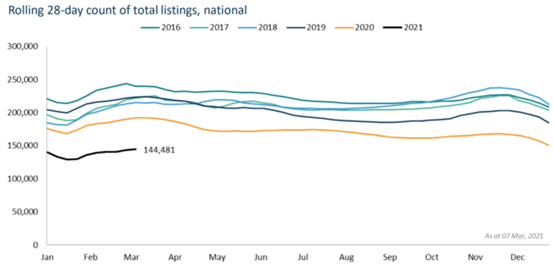

… And Corelogics stock-on-market measure, which shows that the available number of properties is way down on ‘normal’ years.

And that, in a nut shell, is why prices are booming.

Demand is through the roof, and supply is right now due to surging sales activity.

It’s a red hot market. Make no mistake about that.

JG

New “renter’s rights” don’t make sense… until you understand where they’re coming from.

New “renter’s rights” don’t make sense… until you understand where they’re coming from.