Bonds and stocks don’t dance together anymore. It’s a strange new economy.

So I think I’m looking pretty good right now.

Last week, on Wednesday, I said that the US equity market was looking a little bubbly.

By the end of the week, markets had heard the message, and the US market was hammered. Tech stocks were hit hard. Australia followed dutifully behind.

I’m so clever.

But it’s easy to say in hindsight.

And the truth is that markets can look ‘bubbly’ or at least stretched, for ages before something comes along and gives them a nudge.

But last week, something did come along and give markets a nudge.

And that thing was rising bond yields.

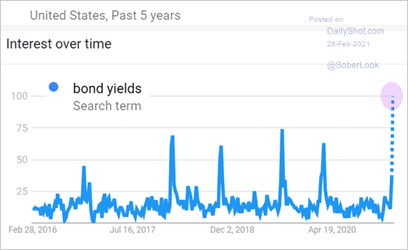

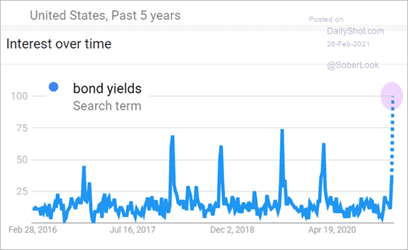

Now someone asked me why rising bond yields would cause stock prices to fall.

That’s a very, very good question.

In fact, that’s a question everyone wants to know right now:

But this is the thing. I don’t think anyone really knows the answer.

In the old days, back when I started investing, my mentor would get out of his horse and buggy and say, stocks and bonds always go in opposite directions.

When stocks go up, bonds go down. When stocks go down, bonds go up.

And it was such a reliable thing that people developed portfolio allocations based on it. Beginning investors were advised to follow Rick Ferri’s Two-Fund portfolio mix: 60% stocks, 40% bonds.

The idea is that bonds would help protect your portfolio in a stock market rout.

Bonds gave you protection.

And they did. It was true for generations. Stocks and bonds would move in opposite directions.

Remember, equities carry risk. Bonds, since they’re backed by the government, carry almost no risk.

And the idea was that in a risk-on environment, people would sell bonds and buy stocks. And in a risk-off environment, they’d sell stocks and buy bonds.

That transfer of demand would cause prices to move in opposite directions.

And that’s what seemed to happen.

Until the QE era kicked in.

After that, there seems to be almost no correlation at all. If anything, stocks and bond prices tend to move together.

(Oh, I’m talking about prices there. In the news you’re hearing everyone talk about ‘rising bond yields’. As a property investor I’m sure you know that if a price falls, and the return remains the same, the yield goes up. So when you hear “rising bond yields” you know we’re also talking about falling bond prices.)

So yeah, last week we saw falling bond prices (and rising yields) AND falling stock prices.

So much for the 60:40 mix.

(You were 100% down on Friday.)

Anyway, back to the puzzle at hand. Bond yields went up, and shares were sold off.

There’s two parts there. What happened to bond yields? And then what happened to shares?

So first, let’s look at why bond yields went up?

The key factor seems to be rising expectations of inflation.

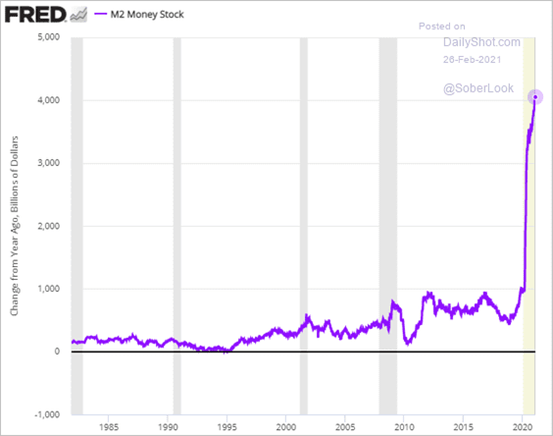

As I’ve noted before, sentiment around the US economy and the Australian economy is pretty bullish right now. That’s on the back of super-cheap interest rates and massive fiscal spending.

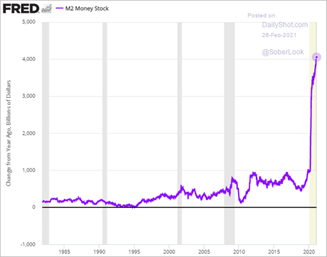

I mean, check out the chart on the US money supply. Totally nuts:

But now, there’s so much money gushing into the system, that people are starting to worry about inflation.

The rate of return on bonds – the yield – has inflation cooked into it. So when inflation, or inflation expectations rise, yields go up.

And so the increase in yields reflects a growing belief that our economies are starting to run a little too hot.

They’re a little too awesome.

Now, that sounds like a good thing for stocks right?

Companies love a hot economy. That’s good for sales right?

But no, stocks got sold off.

And why was that?

Well, to understand that, we have to get to the mystery at the heart of the modern economy. We have to get to the thing that everything hinges on right now.

More on that tomorrow.

“The earlier part of the move was driven by rising inflation expectations because one of the components for bond yields is compensation for inflation,” he said. “More recently, the increase in bond yields has continued and it has come about by an increase in real yields.”

Real yields are the component of the bond yield that is left after investors receive compensation for inflation, and are a good proxy for underlying economic growth expectations.

“If people think that economic growth is going to improve, then real returns – economic growth after inflation – are likely to improve across the entire economy because it’s easier to generate positive returns when the global economy is growing,” Mr Hamlyn said.

Relative yields. – 1.55 T vs 1.51 in equities. Higher yield with zero risk.

Corporate interest burden increases

Discounting

Higher bond yields a negative for gold, since gold doesn’t generate yields.

Discounting

Bond yields, in a way, represent the opportunity cost of investing in equities. For example, if the 10-year bond is yielding 7% per annum then the equity markets will be attractive only if it can earn well above 7%. As bond yields go up the opportunity cost of investing in equities goes up and therefore equities become less attractive.

The yield on bonds is normally used as the risk-free rate when calculating cost of capital. When bond yields go up then the cost of capital goes up. That means that future cash flows get discounted at a higher rate. This compresses the valuations of these stocks.

On the forward rates front, the fed funds futures market is now pricing in more or less a full hike in 2022 as well as two in 2023, and we think the 2022 expectation will be viewed by the Fed as excessive and potentially starting to become problematic.”

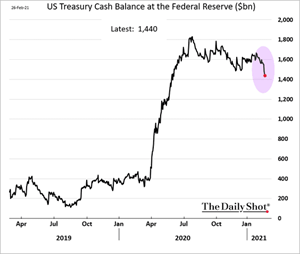

Treasury drawdown = liquidity coming

US Broad money up $3tn y/y

JG

Jon, bond yields are the price of money over 10 years, as the cost rises(yields rise) this impacts the future value of earnings over this period. Unless earnings grow more strongly ( i.e have pricing power ) the value the income streams is diminished and hence the company’s intrinsic value falls. Companies that are price takers are most vulnerable, utilities and low margin businesses. Businesses that have pricing power can offset this effect over the medium term and hence rise after the initial weakness. Technology companies, Materials and cyclical businesses like banks, insurance and building companies.