If the commodity supercycle is all puff, what’s the outlook for property?

So yesterday I told you why many investment banks and economists think we might be on the cusp of a “commodity supercycle”.

That is, they reckon demand has gone ‘new paradigm’ – there’s been a level shift in demand, and supply is going to take years to catch up.

Until it does, commodity prices are going to keep booming, which is awesome for commodity exporters like us, and it will probably feed through into house prices because that’s what always seems to happen.

Yesterday I gave you the four arguments the investment banks are making, but I’m not sure I’m totally buying.

I mean, sure, Commodities prices are booming right now. Absolutely.

But we were always going to get a bit of a rebound as the world recovered from the Covid lockdowns.

And I’m not so sure we’re transitioning into a new paradigm.

I mean, we’re all on the same page in recognising that China’s voracious appetite for commodities cause prices to boom.

China account for 50-60% of iron ore and base metal demand, so whatever they do is going to move the market.

And what they did was go on a massive spending spree to help insulate the economy from Covid. They launched a massive 6 trillion yuan ($1.2 trillion) stimulus package, the equivalent of around 6 per cent of the country’s GDP.

Much of that flowed into the construction sector, helping China’s industrial output – a good indicator of commodity demand – to quickly return to pre-COVID-19 levels.

But now that IP has returned to pre-Covid levels, the Chinese government is taking the foot off the accelerator.

In that sense, much of the stimulus boom has already happened, and it’s not likely to be continued or repeated.

And it’s kind of the same story when you look around the world. Industrial production in the US and Europe has largely recovered all the ground it lost.

So short term stimulus demand may have already peaked.

And the point here is that if the economic recovery really takes off, as a lot of people expect it will, then that will see government stimulus packages start to tapper back.

So you can’t bake in strong recovery demand AND strong stimulus demand. One cancels out the need for the other, and what you get is demand substitution, not demand aggregation.

And when you look at it longer-term, we heard a lot about the Chinese Century a few years ago, but no one really thinks that’s a thing now.

It is true that China went on a massive building spree, and that saw the first mining boom in 2012 to 2014.

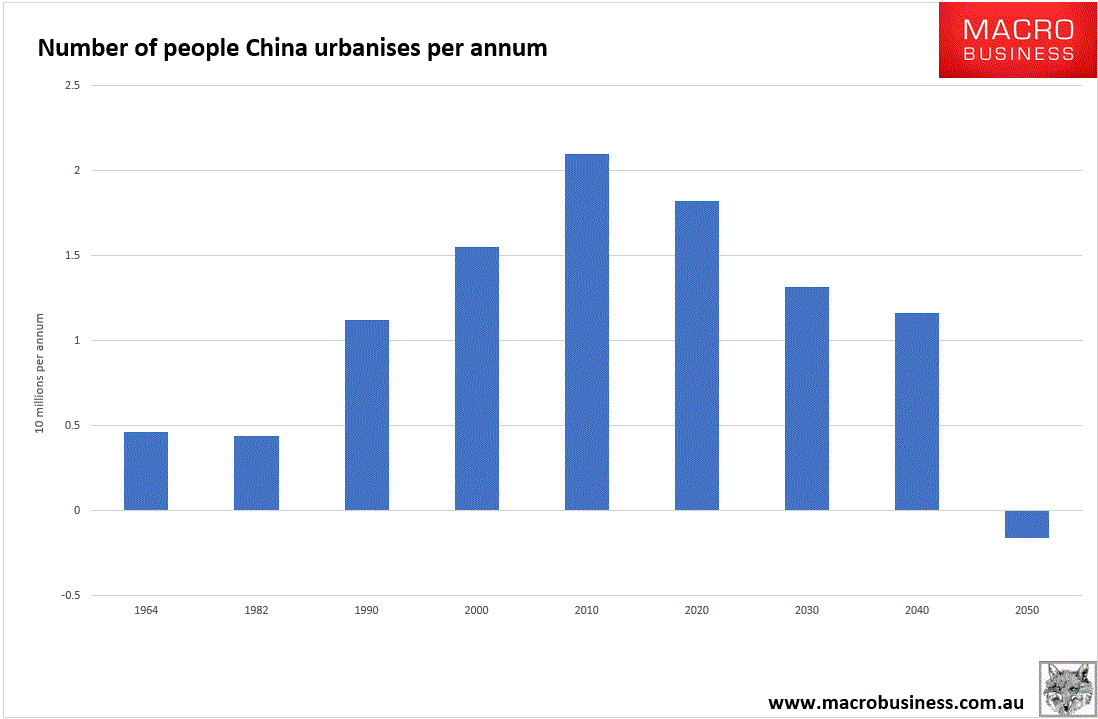

But the consequence of that building spree was a high-rise ghost-tower over-supply that ran well ahead of the nation’s urbanisation needs.

And those urbanisation rates are falling from here on out.

If we assume China reaches 70% urbanisation in 2030 and 80% in 2040, the urbanisation numbers look like this:

So in terms of our supercycle thesis, the urbanisation impulse is waning, not strengthening.

And on the supply side, it might not be so much about limited or fixed supply side capacity, as it was about short-term supply side shocks.

The ongoing trade war with Australia is driving commodity prices higher, but that won’t keep driving them higher. And the price of copper spiked on the back of protests in Peru, and iron ore exports out of Brazil (the number two supplier after Australia) still haven’t recovered from dam collapses and Covid lockdowns.

But the point is, we’re talking temporary rather than permanent factors here.

So I’m not sure we’re talking a permanent level-shift in the supply and demand balance for commodities.

It more looks like a cyclical relfation story, as governments drive the recovery through strong stimulus packages, which just happened to coincide with some shocks to the supply side.

So I’m not sure I’m buying the whole ‘supercycle’ story.

But either way, the next couple of years are looking pretty hot for commodities.

And that in turn will continue to throw heat into the Australian housing market.

Not that the Aussie housing market needs any extra heat right now.

But that’s what we’ve got.

Supercycle or not.

JG