The infamous commodity supercycle didn’t last long…

So one of the key economic themes this year is the idea that we were on the cusp of a “commodity supercycle.”

This was the idea that China and the world were going to spring out of Covid with a massive infrastructure spend, and that was going to create a generational boom in commodities.

That’d obviously be great news for a big commodity exporter like Australia, but I had my doubts.

As I said, way back in March the commodity boom felt more like a temporary bounce-back story. It didn’t seem structural and permanent to me:

… The point is, we’re talking temporary rather than permanent factors here.

So I’m not sure we’re talking a permanent level-shift in the supply and demand balance for commodities.

It more looks like a cyclical relfation story, as governments drive the recovery through strong stimulus packages, which just happen to coincide with some shocks to the supply side.

So I’m not sure I’m buying the whole ‘supercycle’ story.

And where are we at right now?

Well, as of last week, commodities are seeing the sharpest sell-off on record.

Yep. Called it.

From the AFR:

Commodity markets suffered a violent sell-off as mounting anxiety about slower economic growth sent oil and metal prices tumbling and iron ore plunged on weaker steel demand. The Australian currency fell to a 10-month low.

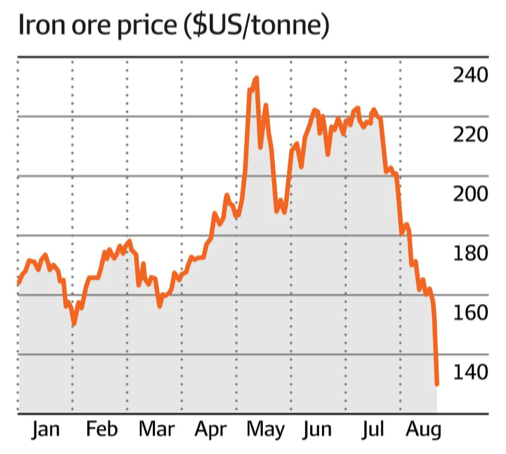

The iron ore price plunged nearly 15 per cent to $US130.2 a tonne and is down 45 per cent from the record high of $US237.57 it reached just three months ago. This continues to weigh on the Australian dollar, which fell 1.2 per cent to US71.5¢ as the risk of the currency falling below US70¢ grew.

Strategists had tipped iron ore’s valuation to ease from elevated levels due to China’s environmental steel production curbs, but the intensity of this pullback – which Morgan Stanley economists said was the commodity’s fastest price correction on record – has pundits rattled.

“We did suspect there was quite a bit of speculation built into the iron ore price when it was above $US200, but the sharp speed of this correction has taken a lot by surprise. When these things burst, they move pretty quickly,” said ANZ senior commodity strategist Daniel Hynes.

“This move goes against the Chinese data we’ve seen so far. While soft, it doesn’t warrant this reaction in prices. This is more about what could potentially happen in the second half, with ongoing restrictions on the steel industry and weaker economic growth.”

The world’s second largest economy is aiming to cut steel output growth this year to 2020 levels. After expanding around 12 per cent in the first half of this year, the country must now reduce steel output by 12.2 per cent from August to December to reach its goal.

This obviously has some big implications for Australia.

Most obviously there’s the impact on the budget. Lower prices for commodities means less economic growth for Australia and less government tax revenue.

And then there’s the impact on Aussie miners like BHP. 80% of their revenue comes from iron ore, so this will rattle them. Their share price is down 10% since they reported their end-of-year results last week, although there are a range of reasons for that.

However, there’s a stabiliser built into the system here that can’t be over-looked.

And that’s the Aussie dollar.

When commodity prices fall, so does the Aussie dollar. As the AFR note, it’s tilting towards US 70 cents.

But a lower dollar is actually good news for Australia. It means our exporters (including miners) are able to sell more for a cheaper price, which gives them a competitive advantage. Local consumers are also encouraged more towards domestically produced goods, rather than imports.

So it’s a good news story for Australia.

And so what we normally get is a fall in the Aussie dollar offsetting a fall in commodity prices.

And we come out about even.

Anyway, I don’t think there’s anything to stress about here.

Other than to say that if that was a commodity supercycle, it’s got to be the shortest on record!

JG.