Secret bank modelling points to a boom for the ages.

I get a bit of access to some insider info every now and then. Not that I’m an insider. I have a mole.

But that mole turns up some gold from time to time.

So let’s have a look at what CBA’s internal model says about the outlook for prices.

The model says, “I’m so hungry. But I look good in jeans. And property is going to boom!”

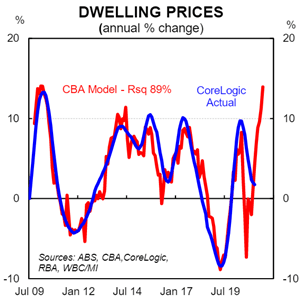

No, it’s a mathematical model. And it charts out like this.

So the model is telling us that prices are very quickly going to go double-digit, and stay there through 2021.

That’s a boom.

It’s the biggest boom since just before the GFC. It even leaves the 13/14 mining-boom driven boom for dead. (Did I mention there’s a mining boom this time too?)

There’s actually not even much speculation here. CBA’s model does a very good job of predicting the near future, because it’s based on things that are pretty reliable indicators – finance, auction clearance rates, things like that.

So they reckon there’s a boom coming. A major boom.

(Not that that’s news to anyone reading my blogs.)

What’s interesting though is that CBA reckon that there’s even some upside risk to this scenario.

The boom could be even bigger:

The key upside risk to our forecasts is sustained exuberance combined with FOMO (’fear of missing out’) which could generate a turbo-charged rise in prices. Indeed we consider this to be the biggest risk to our forecasts given the demand impulse from interest rate cuts, the level of interest rates relative to the rental yield and the recent spike in momentum indicators. History shows that prices can rise very quickly when the housing market is on a roll.

Indeed it may turn out to be the case that the growth profile for price outcomes over the next two years ends up more front loaded than our current projections.

A second upside risk is any further policy changes to boost housing demand such as first-home-owner grants or lower stamp duty (to domestic or foreign buyers). This looks unlikely, however, given the current state of the market.

Finally, if the RBA do not remove or increase the target yield on the 3yr Australian Government bond that would mean that fixed rates are unlikely to drift higher in H2 2021 and 2022 as we expect. However, the risk overall of interest rates being lower than we expect is small given the cash rate is at the effective lower bound, the economy is on an entrenched recovery path and negative interest rates remain, “extraordinary unlikely”.

And their concluding thoughts are something every investor should print out and stick to the fridge right now.

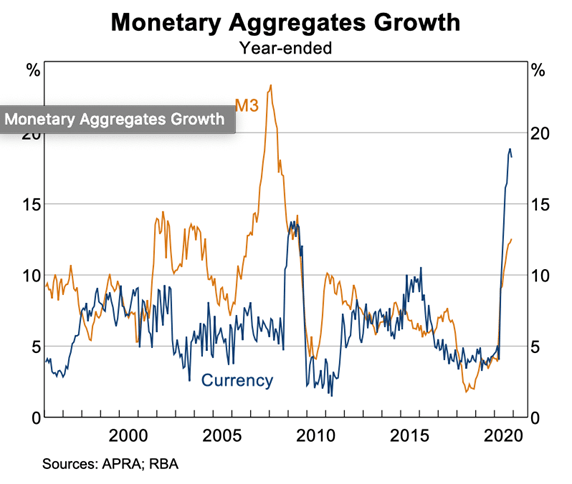

Monetary policy and more specifically the cost of money impacts all asset markets, including housing. The reason that asset prices, including dwelling prices, can seemingly decouple from the economy comes down to largely one thing – central bank policy and changes in the cost of money.

Yup.

And in case you forgot, this chart shows us the pace of money growth speeding up, all thanks to the RBA’s printing press:

Forget what you know.

This boom will be one for the ages.

JG

“Whoa! The banks models say!”

You mean, Jon, model girls working for the banks say something to you?